The Permian’s Next Boom Has a Water Problem

Tens of billions of dollars in AI data center investment is racing toward West Texas. The gas is there. The land is there. The regulatory tailwinds are building. But the constraint that could determine whether this buildout succeeds or stalls has nothing to do with compute. It has everything to do with water.

By Rajendra Ghimire, PhD, MBA | VP, Produced Water Society | VP Business Development, Badwater Alchemy | Managing Partner, FIOPO

Published at ProducedWaterSociety.com | May 2026

Drive west from Midland on Interstate 20 and the evidence of two colliding industries is impossible to miss. Pump jacks work the formation on one side of the highway. On the other, construction crews are breaking ground on facilities that will consume electricity at a scale previously reserved for cities. The Permian Basin, long defined by the hydrocarbons beneath it, is becoming the proving ground for America’s AI infrastructure buildout, and the tension that will define its success is not technical. It is geological, regulatory, and deeply liquid.

THE BET: WHY THE PERMIAN IS BECOMING AI INFRASTRUCTURE GROUND ZERO

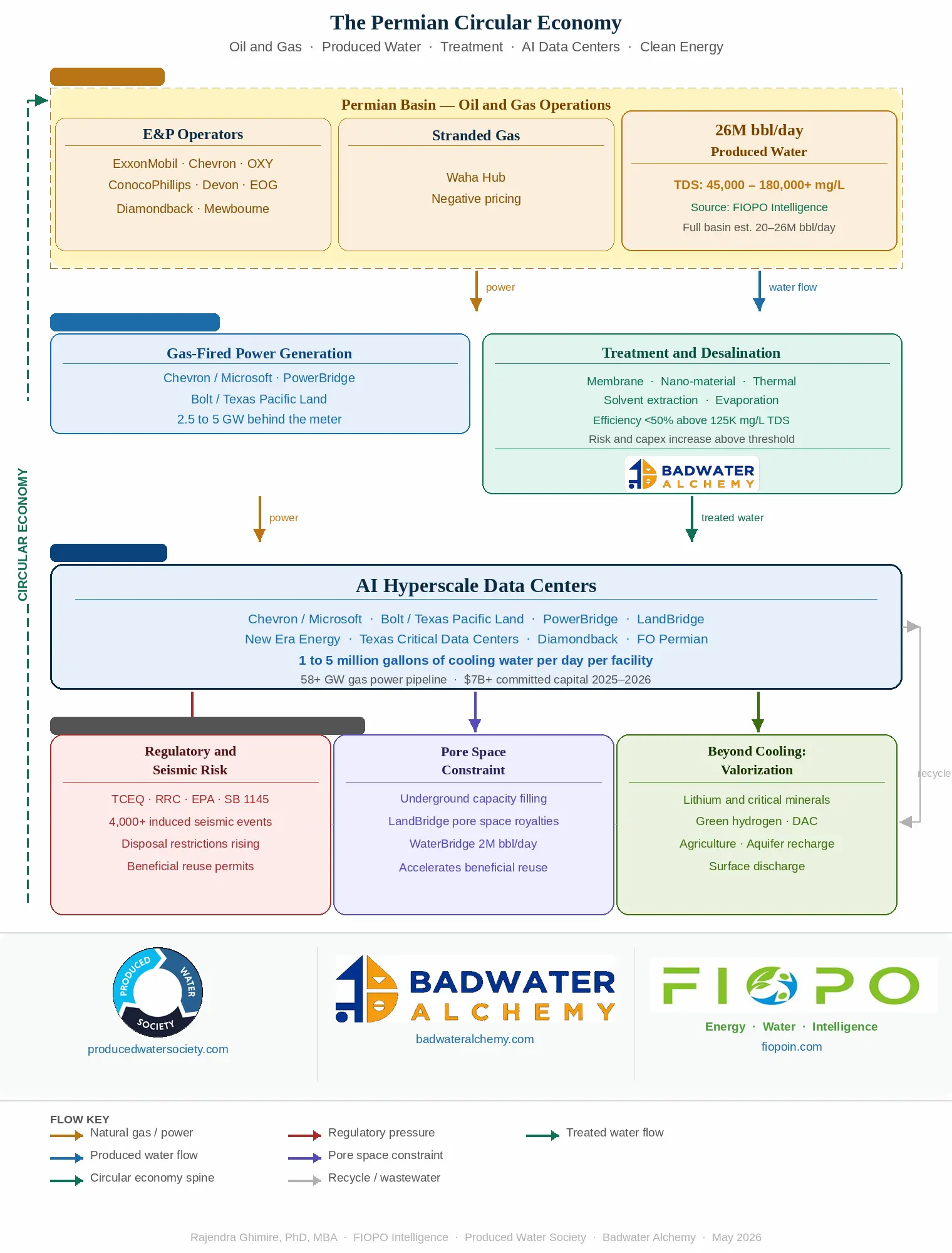

The thesis is straightforward and, in its broad strokes, correct. The Permian Basin produces so much associated natural gas that it regularly overwhelms pipeline egress capacity and trades at deeply negative prices at the Waha Hub in West Texas. Stranded gas that cannot reach markets can power collocated compute cheaply, behind the meter, without waiting years for a grid interconnection queue that is already measured in decades in most US markets.

The announcements have arrived in rapid succession. Chevron disclosed at its November 2025 investor day a 2.5-gigawatt gas-fired power project in Pecos County, expandable to 5 gigawatts, targeting operations in 2027. By April 2026, Bloomberg reported that Microsoft had entered exclusivity negotiations with Chevron and investment firm Engine No. 1 on the facility, the first time a named hyperscaler counterparty appeared in a Permian data center deal. The estimated project cost is approximately $7 billion, making it one of the largest proposed gas-fired power plants in the United States.

On December 17, 2025, Texas Pacific Land Corporation (NYSE: TPL), one of the largest landowners in Texas with approximately 882,000 acres across 20 West Texas counties, announced a strategic agreement with Bolt Data and Energy, a data and AI infrastructure company co-founded and chaired by Eric Schmidt, former CEO and chairman of Google. Under the agreement, Bolt raised $150 million in capital with $50 million invested directly by TPL. In return, TPL received an equity interest, warrants, and a right of first refusal to supply water to Bolt-affiliated projects and related infrastructure. Schmidt’s stated goal: to create the largest and most efficient data center network in the world, anchored in West Texas.

Five Point Energy launched PowerBridge in 2025 with a $1 billion equity commitment, integrating LandBridge’s 315,000 surface acres in the Delaware sub-basin, WaterBridge’s 2 million barrels per day of produced water handling capacity, and fiber connectivity into a single gigawatt-scale offering for hyperscaler customers. New Era Energy and Digital announced a hyperscale AI complex in Lea County, New Mexico with a combined 7-gigawatt generation capacity. Texas Critical Data Centers acquired 235 acres in Ector County for a 250-megawatt AI data center. Diamondback Energy publicly sought data center partners to co-locate on its Permian acreage. During 2025, the pipeline of gas power projects in development in Texas grew by nearly 58 gigawatts of generation capacity, exceeding the peak power demand of California.

| “Our goal is to create the largest and most efficient data center company in the world by combining abundant energy production, efficient and scalable data infrastructure, and the largest land expansion runway in North America.” — Eric Schmidt, Bolt Data and Energy, December 2025 |

THE CONSTRAINT NOBODY IS TALKING ABOUT LOUDLY ENOUGH

Every data center announcement focuses on power. Very few of them address the second critical input with equal rigor: water.

A hyperscale data center requires between one and five million gallons of water per day for cooling. At gigawatt scale, that figure climbs toward tens of millions of gallons daily. The Permian Basin sits in one of the most water-stressed regions in the country. The Ogallala Aquifer is declining. Municipal systems in Midland, Odessa, and Reeves County are already under pressure. Freshwater cannot be the answer. There is not enough of it, and the political cost of directing scarce municipal or agricultural water toward data center cooling would be prohibitive.

The solution has to come from the basin itself. According to RRC Chair Jim Wright, the Permian Basin is producing 5.5 million barrels of oil per day alongside approximately 25 million barrels of water used to pump it. Independent industry estimates applying the basin’s observed three-to-five barrel water-to-oil ratio place current produced water volumes at 20 to 23 million barrels per day, with projections toward 26 million barrels per day by 2030 as drilling shifts into formations with higher water-to-oil ratios. FIOPO’s own intelligence, consistent with current production trends and the full accounting of both unconventional and conventional production, puts the current figure at 26 million barrels per day. Official figures published by the Texas Produced Water Consortium, which cover unconventional wells only, estimate 12 million barrels per day, a number that is widely understood within the industry to undercount total basin volumes. Where the precise number sits in the range of 20 to 26 million barrels per day is less important than the order of magnitude: the Permian is generating over one trillion gallons of produced water per year, the overwhelming majority of which is currently injected back underground at significant cost and measurable seismic risk.

Produced water, properly treated, is exactly the cooling water supply that data centers need. The volumes are there. The infrastructure corridors overlap with data center development zones. The operational footprint is already in place. The question is whether the treatment technology, the regulatory framework, and the commercial structures can move fast enough to meet the demand that is arriving right now.

| The Permian is generating over one trillion gallons of produced water per year. For data centers, it could become the most strategically valuable water supply in North America. |

THE SEISMIC PROBLEM: A RISK THAT CAPITAL CANNOT IGNORE

The produced water disposal system that has supported the Permian’s unconventional production boom is approaching its physical limits, and the consequences are already measurable on seismometers across the region.

Injection of produced water into deep formations has triggered more than 4,000 magnitude 3.0 or greater earthquakes in the Permian Basin, including 10 events above magnitude 5.0, according to USGS data. In the Delaware Basin alone, more than 8,000 earthquakes exceeding magnitude 2.0 have been recorded since 2017. The Texas Railroad Commission has responded by establishing Seismic Response Areas and restricting deep disposal well permits, but the formation pressure continues to build.

Attempts to shift injection to shallower formations have created a different set of problems: well blowouts, ground deformation, and aquifer contamination risks. As RRC Chair Jim Wright acknowledged, “shallow injection alone is not a viable long-term solution.” The University of Texas Bureau of Economic Geology’s Center for Injection and Seismicity Research has characterized the situation plainly: the formation pressure is filling up and there is no quick way to empty it.

For the billions of dollars now flowing into Permian data center development, seismicity is not a theoretical risk. It is a present one. A significant induced seismic event in or near a data center campus, or in a zone where disposal restrictions trigger operational shutdowns, would immediately raise questions about site selection, insurance underwriting, and hyperscaler commitment. Any serious due diligence process must address this directly: if disposal well restrictions tighten further, what is the water management plan? The answer cannot be aspirational. It has to be operational.

| “While a shift to shallow injection has reduced seismicity concerns, shallow injection alone is not a viable long-term solution.” — Jim Wright, Chair, Texas Railroad Commission |

THE REGULATORY OPENING: A WINDOW THAT IS JUST NOW WIDENING

Until recently, the regulatory pathway for treating and beneficially reusing produced water outside of oil and gas operations in Texas was ambiguous at best and commercially prohibitive at worst. That changed materially in 2025.

Texas Senate Bill 1145 consolidated regulatory authority for produced water beneficial reuse under the Texas Commission on Environmental Quality, streamlining permitting and directing TCEQ to develop water quality standards for discharge and land application. House Bill 49 limited tort liability for entities involved in the treatment, transfer, and beneficial use of produced water, removing a major commercial risk that had chilled private investment in treatment infrastructure. The Texas Supreme Court’s June 2025 ruling in Cactus Water Services v. COG Operating clarified that produced water is owned by the mineral operator, establishing clearer ownership that facilitates commercial transactions.

At the federal level, the EPA announced in March 2025 that it would revise effluent limitation guidelines for oil and gas extraction, with Administrator Lee Zeldin signaling the agency will consider expanding beneficial reuse opportunities as treatment technologies become more effective. TCEQ is currently reviewing new discharge permit applications for treated produced water into the Pecos River watershed.

The regulatory window is open. It is not yet fully standardized, and permitting timelines carry real uncertainty. But the direction of travel at both the state and federal level is unambiguously toward beneficial reuse as a commercial and environmental imperative.

THE TECHNOLOGY CHALLENGE: WHEN SALINITY IS THE ENEMY OF EFFICIENCY

Produced water in the Permian Basin is not simply salty. Total dissolved solids concentrations range from roughly 45,000 milligrams per liter in parts of the Cline Shale to well above 100,000 milligrams per liter in deeper formation zones, and in some intervals exceeding 150,000 milligrams per liter. That chemistry profile creates a fundamental engineering challenge that most conventional desalination technology was not designed to address.

Here is the physics that every investor and data center developer needs to understand: as salinity increases, the efficiency of current available and piloted desalination technologies decreases, often sharply. At salinities in the 125,000 to 150,000 milligrams per liter range, the best available and currently piloted desalination platforms operate at roughly 50 percent efficiency at best. Above that threshold, efficiency drops further, energy consumption per unit of treated water output rises steeply, brine management volumes increase, and the compounding risks of scaling, fouling, and system failure grow with each incremental increase in total dissolved solids. Reverse osmosis, the dominant technology at lower salinities, reaches its operational limits well below the concentrations routinely seen in Permian produced water.

This is not a marginal engineering problem. It is the defining economic constraint of the entire produced water-to-beneficial reuse pathway in the Permian. The cost per gallon of treated output rises nonlinearly as you push into the high-TDS ranges that characterize much of the basin’s formation water. Thermal evaporation and crystallization systems can handle higher salinities but carry their own capital cost and energy intensity penalties. The technology landscape is evolving rapidly, with companies from around the world converging on the Permian to deploy or prove their systems, and competitive pressure is driving cost curves down. But the winner in this space will not simply be the technology with the best laboratory results.

| At 125,000 to 150,000 mg/L TDS, the best available and piloted desalination technologies operate at roughly 50 percent efficiency at best. Above that threshold, efficiency drops, energy cost rises, and brine management risk compounds. This is the defining economic constraint of the beneficial reuse pathway. |

THE ACADEMIC VALIDATION: WHAT RESEARCHERS ARE NOW PROVING

The convergence of data center energy systems and produced water treatment is no longer just an industry thesis. It is now an active area of academic research with results being presented at the highest level of the profession. At the 2026 AIChE Annual Meeting, researchers from Oklahoma State University and the Hamm Institute for American Energy are presenting experimental results from a system that directly couples a data center waste heat loop with a produced water treatment unit — precisely the integration this article describes as the commercial opportunity of the decade.

The research, led by Alireza Zahedi, Clint Aichele, and Jason Angolano, starts from two compelling statistics. Global data centers consume 240 to 340 terawatt-hours of electricity annually, with over 75 billion kilowatt-hours per year in the United States alone. Nearly 97 percent of that electricity is ultimately dissipated as heat a continuous, largely wasted energy source that runs 24 hours a day, seven days a week, at every facility. At the same time, produced water from oil and gas operations exceeds 900 billion gallons per year in the United States, making it the largest industrial wastewater stream in the country.

The experimental system uses that low-grade waste heat to drive evaporation and concentration of produced water, reducing brine volume while generating a clean water stream. The results are directly relevant to the Permian Basin data center thesis: the clean water output is suitable for use as cooling tower makeup water in data center operations, closing the loop between the two industries. The concentrated brine is then suitable for downstream mineral recovery ; lithium, salts, and rare earth elements which is precisely the valorization pathway this article’s series will examine in subsequent installments.

The research team monitored clean water production rate, brine concentration factor, temperature profiles, and system stability across varying operating conditions. Their conclusion: waste heat can effectively concentrate produced water while generating a clean water stream suitable for data center cooling reuse. The paper characterizes this integration as a scalable and energy-efficient pathway linking data center energy systems with produced water management, advancing sustainable water reuse and resource recovery from industrial brines.

This research matters for three reasons beyond its technical content. First, it establishes academic credibility for a concept that industry has been discussing but has not yet fully commercialized. Second, the Hamm Institute for American Energy, one of the most influential research organizations in the US oil and gas sector is a co-author, signaling that the industry’s own research infrastructure is now actively investigating this convergence. Third, the framing of the research as a Water Treatment, Desalination, and Reuse session at AIChE means it will be seen by the chemical engineering community that designs and builds treatment systems at scale.

| 97 percent of data center electricity ultimately becomes heat. 900 billion gallons of produced water are generated in the US annually. Academic researchers are now proving these two streams can be coupled to produce clean cooling water and recoverable minerals. The Permian has the highest concentration of both. |

BADWATER ALCHEMY AND THE CASE FOR NEXT-GENERATION DESALINATION

Badwater Alchemy has developed a nano-material based desalination platform specifically engineered for the high-TDS, chemically complex conditions of Permian produced water. The data is validated by EPA-certified laboratories. The value proposition is concrete: higher treatment efficiency and higher throughput at materially lower capital cost per unit of treated water output compared to conventional approaches operating at equivalent salinity levels.

In the context of data center cooling applications, where the economics must close without regulatory subsidy to be commercially sustainable, the capex and efficiency profile of the treatment technology is the difference between a project that pencils and one that does not. Lower capital expenditure per unit of throughput at high salinity is not an incremental improvement. It is a category-level advantage in the specific market segment where Permian data center cooling demand will concentrate.

That said, the technology alone does not determine outcomes in this market. The Permian Basin is a relationship ecosystem as much as a technical one. Operators and midstream companies will pursue the water treatment partnerships that align with their existing infrastructure, financial relationships, and commercial structures. The companies and technologies that get deployed at scale will be those that can close commercial frameworks with the parties who already control the water volumes, the pipeline access, the land, and the regulatory relationships. Technical merit opens the door. Commercial execution, capital alignment, and existing trust relationships determine what gets built.

For more information on Badwater Alchemy’s technology platform and commercial pipeline, visit www.badwateralchemy.com.

THE INVESTMENT THESIS: CIRCULAR ECONOMY AT INDUSTRIAL SCALE

Viewed from sufficient altitude, what is happening in the Permian Basin is not simply a data center buildout or a water management problem. It is the emergence of the first large-scale industrial circular economy in the energy sector, carrying significant implications for how the oil and gas industry is valued, how hyperscalers justify their infrastructure investment, and how institutional capital thinks about the intersection of energy, technology, and sustainability.

The linear model of Permian production generates a waste stream, produced water, that costs money to dispose of, creates environmental and seismic liability, and consumes subsurface pore space at an accelerating rate. The circular model transforms that waste stream into a feedstock: cooling water for the AI infrastructure powered by the same wells. The oil and gas industry becomes not just an energy supplier to the AI economy but a water supplier to it as well.

The financial architecture is taking shape. WaterBridge guides to $420 to $460 million in 2026 EBITDA on $790 million in revenue. LandBridge consistently delivers EBITDA margins above 90 percent. Goldman Sachs raised its LandBridge price target in March 2026 citing expectations of repeatable growth as data center revenue materializes. TPL’s stock surged over 7 percent on the announcement of the Bolt partnership. DigitalBridge Group’s $500 million partnership with Takanock signals institutional conviction that integrated power and water infrastructure in the Permian is a durable asset class.

For hyperscalers, a data center campus powered by stranded gas, cooled by treated produced water, co-located with the oil and gas infrastructure that generates both, with a clear regulatory pathway for beneficial reuse, is categorically different from a facility that relies on the public grid for power and municipal systems for water. It is more resilient, more defensible to ESG scrutiny, and more consistent with the circular economy narrative that shareholders, regulators, and the public increasingly demand.

For oil and gas operators and midstream companies, the stakes are equally significant. A company that can position itself as a water supplier to the AI economy, rather than a liability generator paying for disposal, changes its ESG profile, creates a new revenue stream from an existing operational cost center, and builds a commercial relationship with the technology sector that extends well beyond energy supply.

| The oil and gas industry can become not just an energy supplier to the AI economy but a water supplier to it as well, transforming its largest operational liability into a circular economy asset. That is the sustainability story of the next decade. |

WHAT NEEDS TO HAPPEN: THE FOUR PARALLEL TRACKS

The Permian Basin data center thesis will prove out or fail based on execution across four interdependent tracks. None of them can be solved independently.

Permitting must move at commercial speed. The regulatory framework for produced water beneficial reuse in Texas exists in outline form. TCEQ must translate it into standardized, defensible permit pathways that give data center developers and their capital partners bankable certainty. Pilot study authorization is a necessary step, not a substitute for the full permitting infrastructure that commercial-scale beneficial reuse requires.

Treatment technology must prove its economics at full-salinity conditions. The next twelve to eighteen months will determine which platforms can demonstrate the throughput, consistency, and capital efficiency required to make data center beneficial reuse commercially competitive across the full TDS range of Permian produced water, not just at the lower end of the salinity spectrum.

Commercial frameworks must cross the sector boundary. The transactions that unlock this market are not conventional produced water disposal contracts, and they are not conventional data center water purchase agreements. They are something structurally new: long-term, volume-committed arrangements aligned over the ten-to-twenty-year capital recovery cycles that infrastructure investment requires. Operators and midstream companies will find their way to the technologies and partners that best fit their existing commercial relationships and financial structures. The market will sort this through deal flow.

Seismicity risk must be managed with discipline. The earthquake data from the Permian Basin is a material risk to any data center investment that relies on continued injection well access for water disposal. The regulatory trajectory is toward tighter disposal restrictions. Any investment thesis without a credible, fully funded plan for treatment and beneficial reuse as a substitute for injection is carrying an unquantified tail risk.

THE BOTTOM LINE

The Permian Basin is not simply adding data centers to its existing energy economy. It is constructing the physical infrastructure for a new industrial model, one in which energy production, AI compute, and water management are vertically integrated into a system that is more efficient, more resilient, and more defensible than any of its component parts operating independently.

The capital is arriving. The land is controlled. The power infrastructure is being financed. Operators and midstream companies will pursue the water treatment and commercial partnerships that align best with their existing infrastructure, financial relationships, and strategic priorities. That is how large industrial markets have always worked, and it is how this one will work too.

The companies and individuals who understand the full stack, the water chemistry, the regulatory pathway, the data center cooling specifications, and the commercial structures that bridge the two industries, are the ones who will define what gets built and how fast it scales.

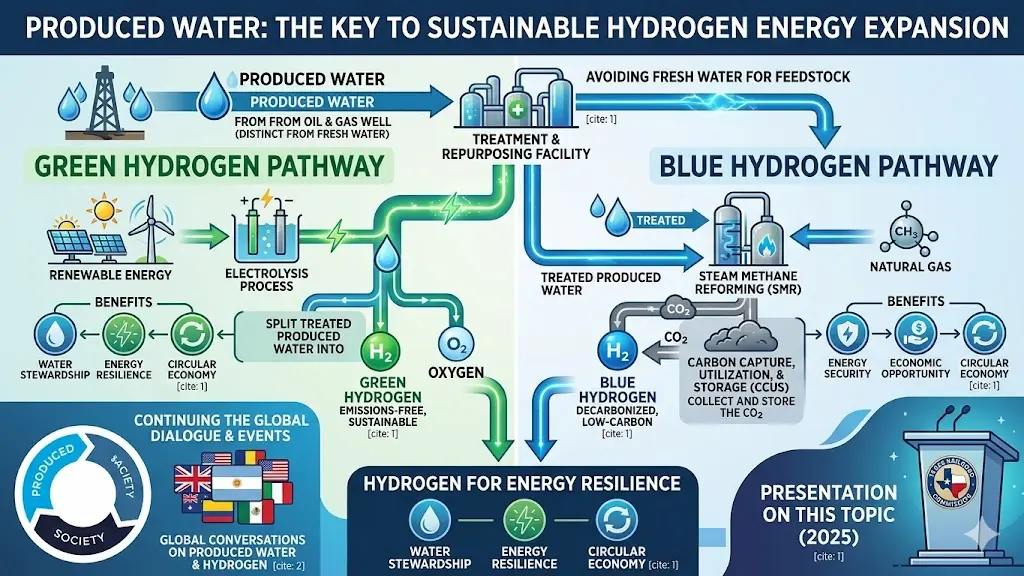

| This is the first in a series of articles on the convergence of produced water, energy infrastructure, and the digital economy. Upcoming pieces will examine the valorization of produced water beyond cooling: the extraction of high-value minerals including lithium and rare earth elements, the pathway to green hydrogen production from treated produced water, and the broader implications for a circular economy in which the energy industry becomes a net producer of critical resources rather than a net generator of waste. |

About the Author

Rajendra Ghimire, PhD, MBA is Vice President and Board Member of the Produced Water Society (30,000 members worldwide), Vice President of Business Development at Badwater Alchemy, and Managing Partner of FIOPO. He has spent fifteen years commercializing produced water treatment and energy infrastructure technologies globally across the US, Middle East, Latin America, and Asia.

rghimire@producedwatersociety.com | producedwatersociety.com | badwateralchemy.com | linkedin.com/in/rajendraghimire

Disclaimer: Disclaimer: This summary was prepared with the assistance of artificial intelligence and, despite human review, may contain errors or omissions. Please verify all information before relying on it for decisions or external communication.

REFERENCES

- Deals and Announcements

- Chevron Investor Day, November 12, 2025. Chevron announces 2.5 GW gas-fired power project in Pecos County, West Texas, expandable to 5 GW, targeting operations 2027.

- Bloomberg, April 2026. Microsoft enters exclusivity negotiations with Chevron and Engine No. 1 on the West Texas data center power project. Estimated project cost approximately $7 billion.

- Texas Pacific Land Corporation (NYSE: TPL) Form 8-K and press release, December 17, 2025. Strategic agreement with Bolt Data and Energy. TPL invests $50 million of $150 million raise; receives equity interest, warrants, and right of first refusal to supply water to Bolt-affiliated projects. SEC filing at sec.gov.

- Data Center Dynamics, October 30, 2025. Bolt Data partners with TPL to develop data center campuses across West Texas. datacenterdynamics.com

- Five Point Infrastructure / LandBridge press release, August 2025. Formation of PowerBridge with $1 billion equity commitment integrating LandBridge (315,000 surface acres), WaterBridge (2 million bpd produced water handling capacity), and fiber connectivity. landbridgeco.com

- High Country News, November 25, 2025. New Era Energy and Digital announces hyperscale AI data center complex in Lea County, New Mexico, with approximately 7 GW combined generation capacity. hcn.org

- Business Wire, February 27, 2025. New Era Helium and Sharon AI announce LOI for 250 MW net-zero AI/HPC data center in Ector County, Texas. Texas Critical Data Centers LLC.

- Data Center Dynamics, March 11, 2026. FO Permian Partners unveils 5 GW off-grid gas power solution for Texas data centers. datacenterdynamics.com

- Oil and Gas Watch, February 19, 2026. Massive gas-powered data center in Permian Basin. GW Ranch project. oilandgaswatch.org

- Texas Tribune, February 2, 2026. Texas environmental regulator issues largest air pollution permit in US history for Fermi America gas power and data center complex. texastribune.org

- GEM Power Tracker cited in Texas Tribune, February 2026. Texas gas power pipeline grew by nearly 58 GW in 2025.

- Produced Water Volumes and Industry Data

- The Center Square, April 9, 2026. RRC Chair Jim Wright, public townhall statement: Permian Basin producing 5.5 million barrels of oil per day and 25 million barrels of water. thecentersquare.com

- Energy News Beat, May 2025. Permian produced approximately 23 million bpd of produced water based on 3 to 5 barrel water-to-oil ratio applied to 6.3 million bpd crude output. EIA crude production data cited. energynewsbeat.co

- Shamrock Precision, May 2026. In 2024, basin produced more than 20 million barrels per day of produced water. Volume projected to reach 26 million bpd by 2030 as production grows and drilling shifts to higher water-to-oil ratio formations. shamrockprecision.com

- Texas Produced Water Consortium (TXPWC) Report to Texas Legislature, 2024. Estimates 12 million bpd for unconventional Permian wells only, with projection to 15 million bpd by 2042. Note: TXPWC figures cover unconventional wells only and do not capture full produced water volumes from conventional and marginal production. texaslivingwaters.org

- JPT / SPE, February 2026. Texas RRC data: produced water flows top 24 million bpd. jpt.spe.org

- World Oil, April 2026. Produced water beneficial reuse projected to increase materially in 2026. worldoil.com

- Seismicity and Disposal

- AAPG Bulletin / GeoScienceWorld, December 2024. More than 4,000 magnitude 3.0 or greater earthquakes with 10 events above magnitude 5.0 as of October 2024. Over 8,000 earthquakes above magnitude 2.0 in the Delaware Basin since 2017. doi.org/10.1306/aapgbull.108.12.2195

- E&E News / POLITICO, December 12, 2025. Produced water injection pressure risks, shallow injection concerns, RRC actions, groundwater contamination risks. eenews.net

- B3 Insight, December 2023. Permian Basin seismic response areas, RRC disposal well restrictions, formation pressure analysis. b3insight.com

- GeoExpro, February 2026. UT Austin Center for Injection and Seismicity Research. Katie Smye, principal investigator. geoexpro.com

- RRC Chair Jim Wright statement on shallow injection: quoted in E&E News, December 2025.

- Regulatory and Permitting

- National Law Review, August 15, 2025. Emerging developments in treatment and beneficial use of produced water in Texas. SB 1145, HB 49, Texas Supreme Court Cactus Water Services v. COG Operating, EPA effluent limitation guidelines revision. natlawreview.com

- BD Law, August 8, 2025. Emerging developments in treatment and beneficial use of produced water in Texas. bdlaw.com

- JPT / SPE, February 2026. Texas explores beneficial reuse as produced water flows top 24 million bpd. TCEQ permit applications for Pecos River watershed. jpt.spe.org

- Railroad Commission of Texas, January 8, 2024. Produced Water Beneficial Reuse Framework for Pilot Study Authorization. rrc.texas.gov

- Texas Tech University / Texas Living Waters, March 2025. Oil and Gas Produced Water in Texas. texaslivingwaters.org

- Technology

- Zahedi, A., Aichele, C., and Angolano, J. (2026). Coupling Data Center Waste Heat with Produced Water Treatment for Energy-Efficient Water Reuse and Resource Recovery. Presented at the AIChE Annual Meeting 2026, Water Treatment, Desalination, and Reuse: Processes session. Oklahoma State University and Hamm Institute for American Energy. aiche.confex.com/aiche/2026/prelim.cgi

- AIChE Annual Meeting 2026, similar papers cited in the same session: (a) Gao et al., A Data-Driven Classification and Optimization Framework for Mineral Resource Recovery from Concentrated Brine, Rowan University and CSIR-CSMCRI; (b) Nyamekye and Trembly, Valorization of Produced Water via Controlled Strontium Carbonate Synthesis for Thermochemical Energy Storage Applications, Ohio University; (c) Gilvan Neto et al., Data Center Cooling via Zeolite-Based Thermal Energy Storage and Waste Heat Recovery, NYU Tandon School of Engineering, University of Delaware, and MIT Energy Initiative. aiche.confex.com/aiche/2026/prelim.cgi

- SPE / Journal of Petroleum Technology, October 2025. Scaling treated produced water for data center cooling in the Permian. jpt.spe.org

- Davis Graham and Stubbs, April 1, 2026. US Produced Water: The Emerging Value Chain Reshaping Energy, Water and Critical Minerals. Tetra Technologies Oasis platform, EOG pilot. davisgraham.com

- Chemstar Water, November 2025. West Texas data centers and produced water treatment. chemstarwater.com

- Energy Crisis Substack, July 7, 2025. Water, West Texas, data centers. WaterBridge operational data, Texas Supreme Court ruling, DigitalBridge. energycrisis.substack.com

- Investment and Infrastructure

- International Business Times Australia, April 10, 2026. LandBridge stock surges on 2 GW data center deal. Goldman Sachs price target raised to $84. ibtimes.com.au

- Seeking Alpha, March 18, 2026. WaterBridge Infrastructure, LandBridge comparison. WaterBridge 2026 EBITDA guidance $420 to $460 million on $790 million revenue. seekingalpha.com

- 310 Value Substack, December 19, 2025. Data Centers in the Permian Basin Part 3. LandBridge, WaterBridge, Chevron project, TPL analysis. 310value.substack.com

- Electron Economics Substack, May 2026. The Permian data center thesis is real. Chevron, Microsoft, Engine No. 1 details. electroneconomics.substack.com

- Engineering News-Record, November 16, 2025. Chevron to build first data center power plant in Texas Permian area. enr.com

- The Real Deal Texas, December 18, 2025. Eric Schmidt-backed firm teams up with Texas Pacific Land. therealdeal.com

- Commercial Property Executive, December 18, 2025. TPL and Bolt team up to develop West Texas data centers. commercialsearch.com

- Simply Wall St, February 11, 2026. LandBridge pivot to pore space royalty. simplywall.st